Can I Afford A House? The Shocking Truth About Your Budget

Let’s be honest, property browsing is fun, but it inevitably raises the biggest question: Can I afford a house?

Setting a budget is quite confusing for most people because of the financial terms surrounding it.

Nevertheless, you do not need financial knowledge in order to plot your route.

It is a combination of knowing how your money comes in and goes out, understanding what lenders like, and spotting extra costs early on.

By dividing the figures into small parts, you will be able to go on without any doubts at all.

Depth-wise, let’s first understand mortgages, the requirements for deposits, and the disclosure of additional fees.

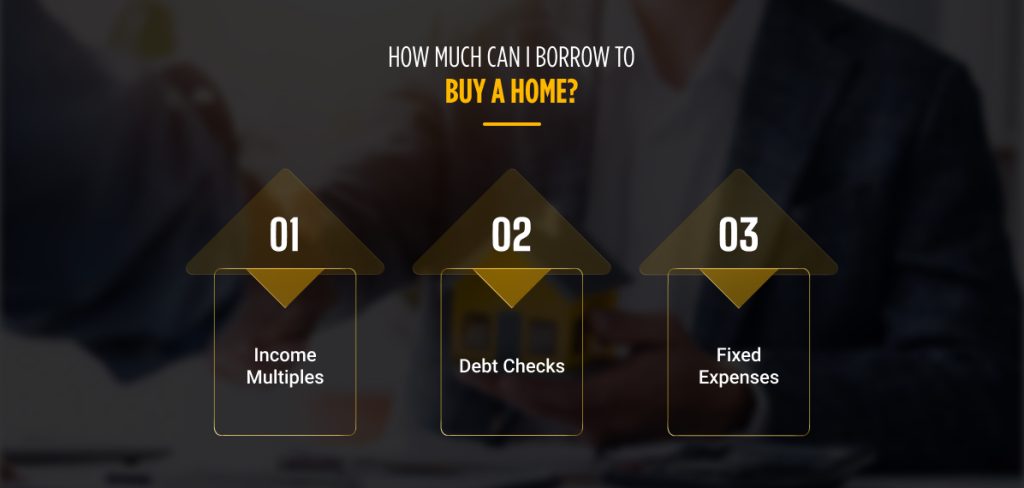

How Much Can I Borrow To Buy A Home?

When you begin the search for a property, figuring out how much you can borrow is your first step.

Most banks base this on a few key aspects of your financial situation.

- Income Multiples: Most lenders might be willing to lend you four or five times the amount of your yearly salary.

- Debt Checks: Lenders will likely reduce your loan amount if you have credit card debt or car loans.

- Fixed Expenses: Steady costs like childcare or subscriptions will affect your final offer.

In fact, each bank has its own unique way of calculating the amount.

Using an online calculator or discussing your needs with a mortgage broker is a wise decision to get a precise, tailored figure.

What Deposit Do I Need To Buy A House?

Gathering the money for a deposit is a major part of working out whether I can afford a house. It is basically the upfront cash that you hand over to get your property.

Most of the time, you are asked to put down a deposit of at least 5% of the total house amount.

In other words, if the house that you want costs £250, 000, your absolute minimum deposit would be £12, 500.

But, of course, it is much better to go for a higher deposit. Not only will a larger down payment allow you to tap into a wider pool of lenders.

However, it will also offer significantly lower monthly mortgage rates.

According to the latest publication from Halifax, the typical first-time buyer made a substantial 20% deposit, which averaged about £ 61,090.

If that intimidates you, don’t fret. Currently, there exist several low-deposit schemes to consider:

- Mortgage Guarantee Scheme: This scheme, among other things, can help you buy a home with as little as a 5% deposit, assuming you are earning a regular income and have a good credit record.

- Deposit Unlock: The focus of this offer is on new builds, where the buyer only has to put down as little as 5% deposit.

Where does this money actually come from? Most of the folks put it together from several different sources:

- Market a Present House: Capitalize on one’s existing property.

- Personal Savings: Putting away little by little through budgeting.

- The Bank of Mum and Dad: Receiving a monetary gift from family members.

- Guarantor Mortgages: In this scenario, parents can offer their income or property as collateral. However, they will be held liable if you default on payments.

Will I Be Able To Afford The Monthly Payments?

Getting the loan is just one part of the story; the real issue is your ability to make the loan repayments comfortably every month over the long run.

After all, you want to be happy in your new home, not burdened by stress over it.

- The 35% Rule: Generally, you shouldn’t spend more than 35% of your net income on mortgage payments.

- Rent vs. Mortgage: It is worth bearing in mind that the funds you have been using for rent are now being redirected towards paying off your mortgage.

- Rate Choices: The big decision is whether you prefer the peace of mind that comes with a fixed rate or the potential to save with a variable rate.

Keeping a balanced budget is the first step to avoiding the feeling of being “house poor” in the future.

If you want to be more certain about things, consulting a fee-free mortgage adviser is a great way to both remove uncertainty and gain a clearer picture.

How Much Are The Extra Costs Of Buying?

Loads of first-time buyers tend to overlook that buying a property entails expenses other than just the price they pay for the house.

Actually, additional charges might amount to as much as 10% of the total amount you pay for the house.

- Stamp Duty: This tax on real estate changes based on the region you reside in and whether you are a first-time buyer.

- Legal Fees: You have to pay a solicitor or a conveyancing firm for the legal work they carry out.

- Surveys & Moving: Property inspections are a way to identify hidden defects in a property.

Apart from that, there are costs associated with using trucks for moving.

Since these costs arise long before you get your furniture, it is highly important to include them in your budget from the beginning.

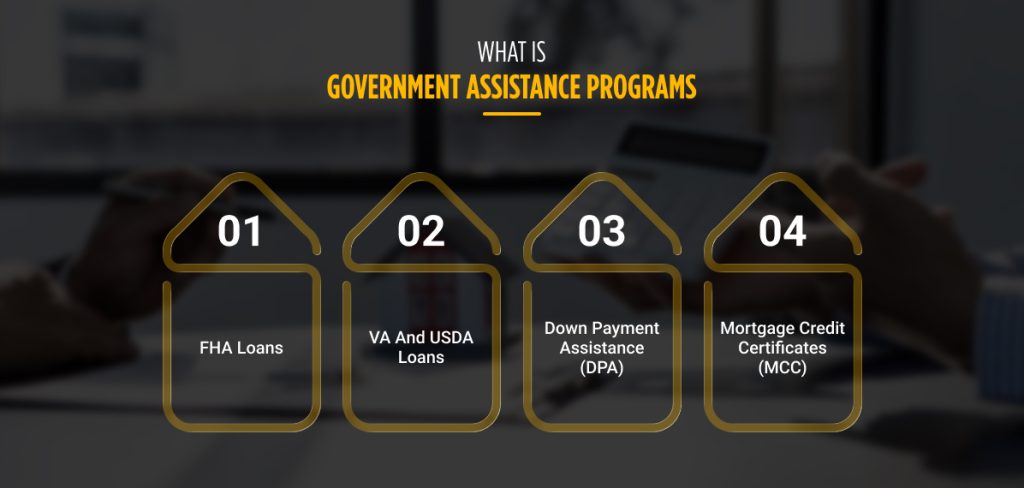

Government Assistance Programs: Can I Afford a House?

If you are wondering, “Can I afford a house?” a number of government programs in the US may be able to help you get a home without the need for a big cash down payment.

· FHA Loans

With backing from the Federal Housing Administration, the loans require only a 3.5% down payment, and credit requirements are quite flexible.

So they are very suitable for first-time homebuyers.

· VA And USDA Loans

If you are eligible, you may get 0% down payment. VA loans are for military families, and USDA loans are for buyers in suburban and rural areas.

· Down Payment Assistance (DPA)

Many states and localities will give you a grant or a forgivable loan to pay your down payment or closing costs.

For example, Florida’s Hometown Heroes can offer up to $35, 000 to teachers and healthcare workers.

· Mortgage Credit Certificates (MCC)

Through this program, part of your monthly mortgage interest is given back to you as a federal tax credit, so you end up saving money each year.

Therefore, taking advantage of these options greatly lowers your financial barrier to homeownership.

Leave A Reply