Is Property Investment Uk Still Worth It? The Honest Truth Landlords Won’t Tell You!

Are you thinking about making your money work harder for you? Well, you are not alone.

Getting into the housing market is one of the most popular ways to build wealth.

However, it is important to know the ropes before you dive in.

Whether you want to pocket some extra cash each month or build a nest egg for the future, here is a simple, stress-free guide to property investment UK and how it all works.

Why Think About Property Investment in the UK?

Investing in bricks and mortar is a classic way to make your money work harder.

Essentially, it offers two big wins. First, you get a regular monthly income from tenants paying rent.

Second, your investment can grow over time if house prices go up. In fact, a solid goal for a property investment UK return is around 5% to 7% each year.

On top of that, many families use property to help out the next generation. For instance, buying a home for a child can give them a massive head start.

Best of all, property is easier to understand than complex stock markets. You can see it, touch it, and easily grasp how it makes money.

The Realities And Risks

However, it is not all smooth sailing. Buying a house comes with high upfront costs like taxes, legal fees, and maintenance.

This is why it might take months or even years before you see real profit.

Furthermore, recent changes to tax laws mean landlords earn less than they used to.

Simple and Friendly Ways to Master Property Investment UK

When it comes to property investment UK choices, you have several exciting paths to choose from.

Let’s break down the five most popular ways to get started, keeping things simple and straightforward.

1. Buy-To-Let (The Traditional Route)

Buying a property to rent out to long-term tenants is a classic move. In fact, around 4.6 million homes in the UK are rented out this way!

If you do not have a mountain of cash, you will need a specific buy-to-let mortgage.

Just keep in mind that these loans usually require a larger deposit and higher interest rates. These are typically higher than those on a normal home loan.

It is not quite as easy to make a profit as it used to be, because of recent tax hikes and rising interest rates.

Always remember: your home may be repossessed if you do not keep up with your mortgage repayments.

2. Property Development (Fixer-Uppers)

If transformation is your thing, this one is for you. This involves

- Buying a run-down property,

- Fixing it up (or adding an extension)

- Selling it quickly for a profit.

You can even get special renovation mortgages to help cover the build costs.

However, you need to budget incredibly carefully so unexpected building costs do not swallow your profits.

3. Holiday Lets (The Staycation Boom)

You can buy a property in a beautiful holiday spot and rent it out to travellers, instead of renting to long-term tenants.

This has become a very popular alternative to traditional buy-to-let because it can offer great returns.

Plus, you get a beautiful holiday home to enjoy yourself when guests are not staying there! You will need a specialist holiday let mortgage for this route.

4. Buying Property Abroad (Sunshine And Rentals)

Buying overseas lets you own a slice of paradise that you can rent out to tourists and eventually retire in.

However, it might feel really tricky to navigate foreign laws, and language barriers can be challenging.

It is smart to work with a UK-based bank or a specialised mortgage broker who knows the local market inside out. This can help to keep things safe.

5. Property Funds (The Hassle-Free Option)

You can invest in a property fund instead if you do not want the headache of managing tenants or fixing leaky roofs.

Vehicles like Real Estate Investment Trusts (REITs) let you buy shares in large property projects through the stock market.

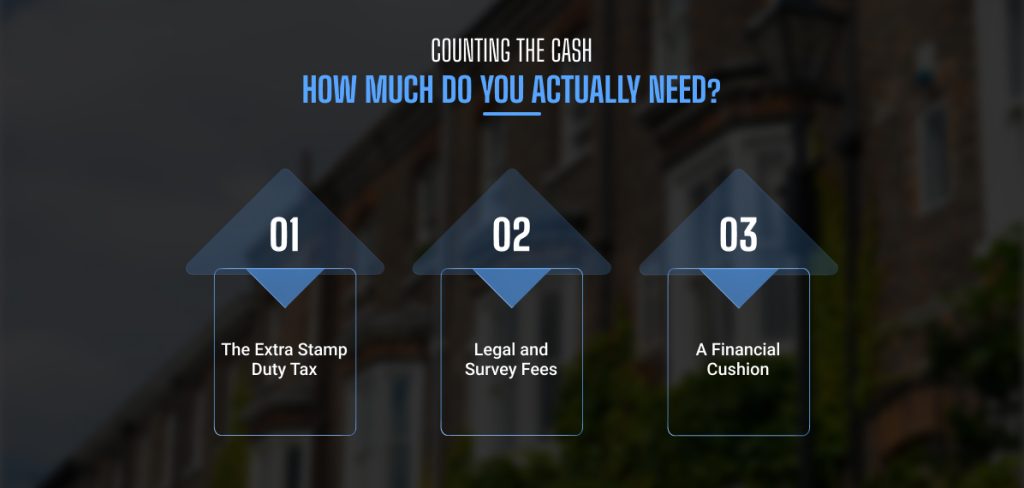

Counting the Cash: How Much Do You Actually Need?

Property investment in the UK requires a fair bit of upfront cash, along with just a nod and a handshake.

Your biggest hurdle will be the deposit, unless you can buy a place outright. This is unlike buying your own home.

Lenders usually want a minimum deposit of 25% for a rental property.

For example, if you buy a house worth £300,000, you will need to find £75,000 in cash right away.

On top of that, you need to budget for these essential extras:

· The Extra Stamp Duty Tax

Buying a second property triggers an extra tax if you already own a home. The stamp duty rate for additional properties is 5% higher than the normal rate.

On that same £300,000 investment property, your tax bill jumps from a standard £2,500 up to a hefty £17,500!

· Legal and Survey Fees

You will need a conveyancing solicitor to handle the legal paperwork. Plus, it is smart to get a house survey done so you do not buy a money pit.

Moreover, a standard RICS Level 2 survey on a £300,000 home usually costs between £600 and £700.

· A Financial Cushion

Lastly, you must keep a cash safety net. This money covers unexpected repairs, landlord insurance, mortgage fees, and periods when the property is vacant.

Location, Location: Where Should You Buy?

Finding the right spot is everything. Prime locations across the country include London and buzzing major hubs like Birmingham, Manchester, and Leeds. Areas near universities are also great because students always need housing. However, if you rent to multiple independent tenants (known as a House in Multiple Occupation, or HMO), you will have to jump through a lot more legal hoops.

Before you buy, talk to local estate agents to see what types of properties are actually in demand. You can also use online rent calculators to see if the local rental income will realistically cover your costs.

What About New Builds?

Buying a brand-new home sounds easy, but be careful. New builds can drop in value during the first few years, much like a brand-new car driving off the lot. They can still be a great option, but only if you negotiate a great price and plan to hold onto the property for the long haul.

Weighing Up The Good And The Bad

Before taking the plunge, it helps to look at both sides of the coin.

The Perks (The Good News)

- Steady Cash: You get a lovely monthly income from rent, if you manage it well.

- Long-term Growth: You get to watch your investment grow over the years as house prices rise.

- Family Support: It is a brilliant way to secure a future home for your kids.

The Pitfalls (The Risks)

- Pricey Mortgages: Buy-to-let loans have higher interest rates and steep setup fees.

- Slow Profits: Your investment has to work incredibly hard to break even in the first few years. This is because the startup costs are so high.

- Tenant and Maintenance Drama: Boilers break down, and sometimes you get difficult tenants who drain your time and money.

- Tricky to Sell: Selling a house takes time. Furthermore, UK tenancy laws (such as the Renters’ Rights Bill) protect tenants.

This means you cannot easily evict someone just because you want to sell the house in the first 12 months. - Capital Gains Tax: When you finally sell your rental property, you will usually have to pay tax on the profit you made.

How Do Rental Mortgages Work?

A buy-to-let mortgage is quite different from a normal home loan. Banks look at how much rent the property can generate, instead of looking at your salary. However, you might still need a backup salary of at least £20,000 to £25,000 to qualify.

Most banks want the monthly rent to cover at least 125% of your mortgage payment.

Many landlords choose an interest-only mortgage. This can help keep costs down.

Moreover, the strategy also keeps your monthly payments low.

However, always remember that you are not paying off the actual debt, so you will still owe the full loan amount at the end.

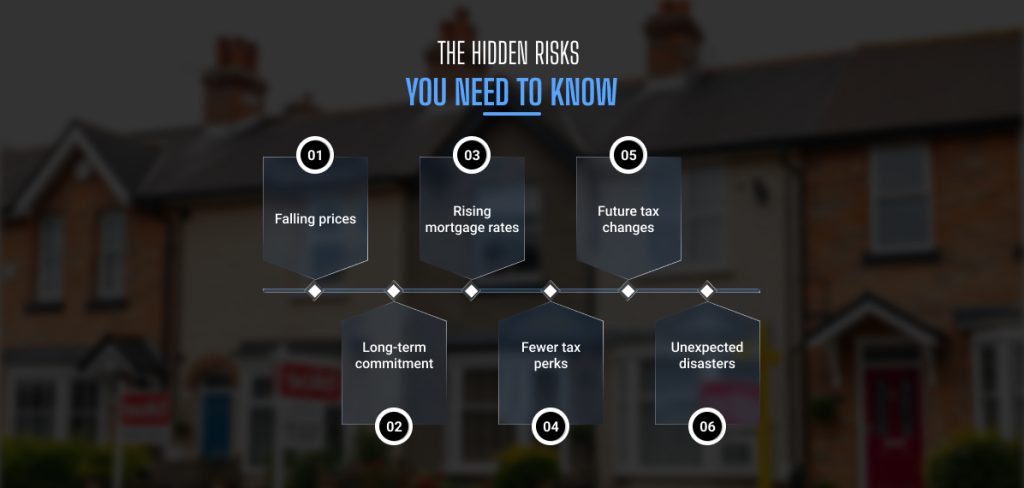

The Hidden Risks You Need To Know

While a property investment UK can build great wealth, it is not a guaranteed win. Several hidden risks can quietly shrink your returns if you are not careful.

Here are the key risks you need to keep in mind:

- Falling prices: Property values and rental demand can suddenly drop.

- Long-term commitment: You must stay invested for years to break even.

- Rising mortgage rates: Higher interest rates will quickly eat your profits.

- Fewer tax perks: Landlords can no longer fully deduct mortgage interest.

- Future tax changes: Government budgets could increase your future tax bills.

- Unexpected disasters: Unpredictable issues, such as cladding crises, can occur at any time.

The housing market moves in cycles, so never invest cash you cannot afford to lock away.

Your Beginner’s Guide To Yields And First Steps

When planning your property investment journey in the UK, aiming for a 5% to 7% return is a great benchmark.

However, this figure varies by area. For instance, you might see lower returns in expensive spots such as London. However, higher yields in cheaper northern cities.

Interestingly, you can actually buy a rental property even if you are a first-time buyer.

If your local area is too expensive, buying an investment property somewhere cheaper is a clever way to get onto the ladder.

Keep in mind that not all banks offer these loans to newbies, so working with a mortgage broker is vital.

Additionally, if you buy a rental first, you will lose your first-time buyer Stamp Duty tax discount when you eventually buy your own home.

How To Get Started: 4 Simple Steps

So, are you ready to take any action? Well, here is how to kick off your investment journey:

- Pick your strategy

First, you need to decide if you want a long-term rental, a holiday let, or a fixer-upper.

- Calculate the yield

After that, calculate your annual profit by dividing your annual rent by the purchase price.

For example, a £200,000 house making £10,000 a year in rent gives you a 5% yield.

- Do your homework

Thirdly, you can conduct research on what local tenants are actually paying for similar houses nearby. If you are renovating, get firm quotes from builders before buying.

- Value your time

Managing tenants is hard work. You can pay an estate agent to handle it, or use budget-friendly online platforms like OpenRent to set up contracts cheaply.

Leave A Reply