Buying Vs Renting A Home: The Hidden Costs And Real Truth They Don’t Tell You About Real Estate

In 2026, there will be an ongoing debate in the UK: buying vs renting a home. Now, renters love the freedom and spontaneous nature of renting.

However, due to rapidly rising prices, this provides fewer accommodations than buying does.

According to ONS statistics, average private rent in the UK has hit a record high of £1,381 a month (up 3.5% from last year).

Buying becomes even more important when you factor in the additional costs of financing your purchase through borrowing, which is necessary!

The current rate for 5-year fixed mortgages ranges between 4.89% and 5.23%, depending on your deposit size, according to Rightmove’s mortgage tracker.

However, according to Homeowners Alliance statistics, renters spend 34% of their income on housing-related expenses, compared to 18.7% for homeowners.

The first step is to determine how much you’ve saved.

Can You Afford Your Own Place?

If you are trying to decide whether to rent or buy a house, the first step is to determine what you can afford to spend.

You will have decided to rent if housing prices are too high for buying to be a reasonable option at this time.

Otherwise, you may be thinking about purchasing a home in the future with cash.

In addition, even if you can afford to purchase a home now with your own cash, you might decide to rent until you are certain of your housing needs and commitments.

They would prefer the benefit of less financial responsibility when renting than when owning their own home.

What Government Help is Available to Help You Buy a Home?

You can try government programs if you want to buy a property. These initiatives can really simplify changing from buying vs renting a home by greatly reducing the initial payment.

Below are some main ones you can get:

- Low Deposit Schemes: The Mortgage Guarantee scheme allows you to buy a home with only a 5% deposit.

- First Homes Discount: Starting buyers will be offered 30% to 50% off the market price for newly built homes.

- Shared Ownership: This method allows you to buy a share of a home and pay rent on the remaining share.

- Lifetime ISAs: Special tax-free savings accounts are topped up with a free government cash bonus.

So these schemes close the gap if you are having difficulties with high property prices.

They can be a great support in helping you transition to homeownership without any problems.

Buying Vs Renting A Home: What Are The Advantages Of Buying Your Own Home?

When you’re deciding between buying and renting a home, owning your place definitely comes with clear advantages that renting just cannot offer.

Let’s take a closer look at why buying a home can be a really good move for both your lifestyle and your finances.

1. More Freedom And Feeling Secure

Complete Creative Control: Since it’s your property, you can do whatever you want. Paint the walls, remodel the kitchen, or change up the garden—no need to ask a landlord for permission.

Pet-Friendly Living: You will not have to stress about strict “no pets” rules or paying extra monthly fees for your pets.

No Surprise Moves: You’re completely safe from sudden evictions or getting a last-minute request to move out.

Better Well-Being: Studies show that 91% of homeowners feel their property makes them happier and less stressed, compared to just 79% of renters.

2. Saving Money In The Long Run

Landlords can raise the rent every year. But with a fixed-rate mortgage, your main housing payment stays predictable for many years.

Can Be Cheaper Than Renting: When interest rates are stable, your monthly mortgage payment is often less than what you’d pay in rent for a similar home in the area.

Building Your Own Investment: Your monthly payments are like putting money into a forced savings account.

Instead of paying off your landlord’s debt, you’re building up ownership in something that belongs to you.

3. Building Real Wealth

Historically, home values tend to increase over time. For most people, their home increasing in price is the biggest way they build wealth during their lives.

Future Rental Income: If you move away for a while, you can rent out your property and get a steady income without doing much work.

A Built-In Retirement Plan: Your home can be like a financial safety net for your retirement.

When you stop working, you can sell your big house, buy a smaller one, and live comfortably with the money you made.

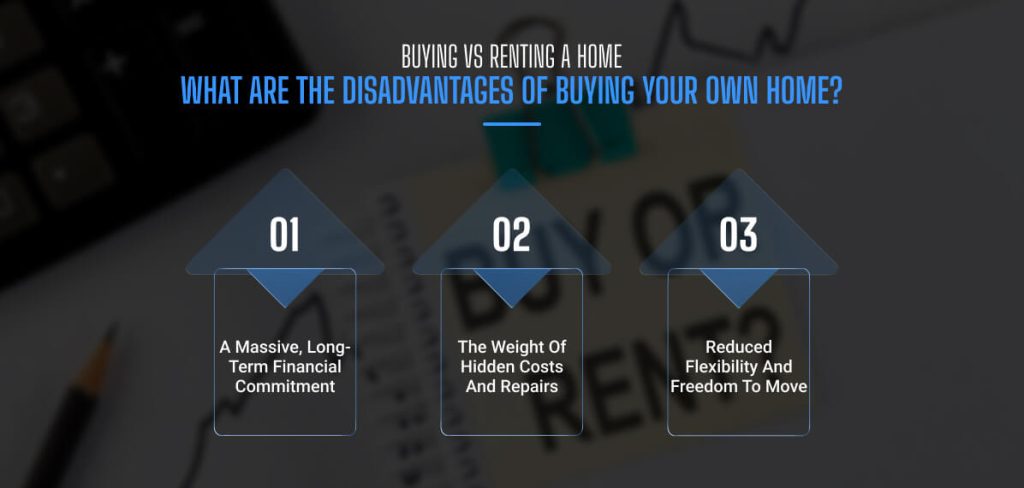

Buying Vs Renting A Home: What Are The Disadvantages Of Buying Your Own Home?

While ownership sounds amazing, it is also a heavy financial responsibility. To make an informed choice, you must look closely at the potential risks and downsides.

1. A Massive, Long-Term Financial Commitment

A mortgage is a 25 to 30-year contract. It is usually the largest financial obligation you will ever take on.

Risk of Foreclosure: If you lose your job or suffer an illness and cannot pay your mortgage, the bank can repossess your home.

The Trap of Negative Equity: If property prices drop, you might end up owing more to the bank than the house is worth, making it impossible to sell or move.

2. The Weight Of Hidden Costs And Repairs

When the boiler breaks, the roof leaks, or a pipe bursts, there is no landlord to call. You must find the repair technician and pay the bill.

You might also have to pay the ongoing overhead costs. As an owner, you must pay for building insurance, annual maintenance, and local property taxes, which can add up quickly.

3. Reduced Flexibility And Freedom To Move

Selling a home takes months and costs thousands in agent fees, legal paperwork, and closing costs.

If you get a job offer in another city or want to travel, you cannot just give 30 days’ notice and walk away. Buying is risky if your life or career is still changing.

Leave A Reply