How Long Does It Take To Get Preapproved For Mortgage: Pre-Approved Home Loans Basics

It always feels surreal when you find your dream home, and the seller accepts your offer! However, you still have a few steps to cross before getting the keys.

You might even wonder, how long does it take to get preapproved for mortgage paperwork?

Now, typically, getting pre-approved takes just 1 to 3 days. And that is only possible if you have your tax returns and pay stubs ready.

After that, final loan approval usually takes about 30 to 45 days.

Thus, you have to ensure the following things to keep things moving smoothly,

- Firstly, you have to respond promptly to your lender when they request documents.

- Secondly, you can avoid new debt. This can be about buying a car or opening new credit cards, which can cause major delays.

Once you can understand the timeline, it helps you relax and enjoy the journey to your new home!

How Long Does It Take To Get Preapproved For Mortgage?

Normally, the final mortgage approval takes about 30 to 60 days. However, you can speed this up significantly.

You can actually close your dream home in just two to three weeks after your offer is accepted, if you get pre-approved before house hunting.

Consequently, you might wonder: how long does it take to get preapproved for mortgage paperwork? Luckily, it usually takes just a few days.

You and your lender get the hard part out of the way once you start doing the extra work up front. And as a result, you can shop with total confidence.

On top of that, the sellers will love you because they know your finances are solid. This is what makes your entire homebuying journey much smoother!

Critical Distinction: Pre-Qualification vs. Pre-Approval

Many first-time homebuyers confuse these two terms, but lenders treat them very differently:

| Pre-Qualification | Pre-Approval |

|---|---|

| An informal, preliminary estimate of what you can borrow. It is based entirely on self-reported financial data and takes only a few minutes but carries no legal weight. | A formal, conditional commitment from a lender. It requires a hard credit check and verifies documentation, giving you the power to make serious offers on homes. |

The Essential Pre-Approval Document Checklist

To guarantee you get your pre-approval within the 1-to-3-day window, gather these exact documents before speaking to a lender:

- W-2 forms from the last two consecutive years.

- Federal tax returns (complete schedules) over the past two years.

- Most recent pay stubs cover the last 30 days.

- Bank statements for all checking and savings accounts (past 60 days).

- Quarterly statements for investment assets (401k, IRA, or brokerage accounts).

- A valid photo ID (Driver’s license or passport).

- A signed gift letter if family members are helping fund your down payment.

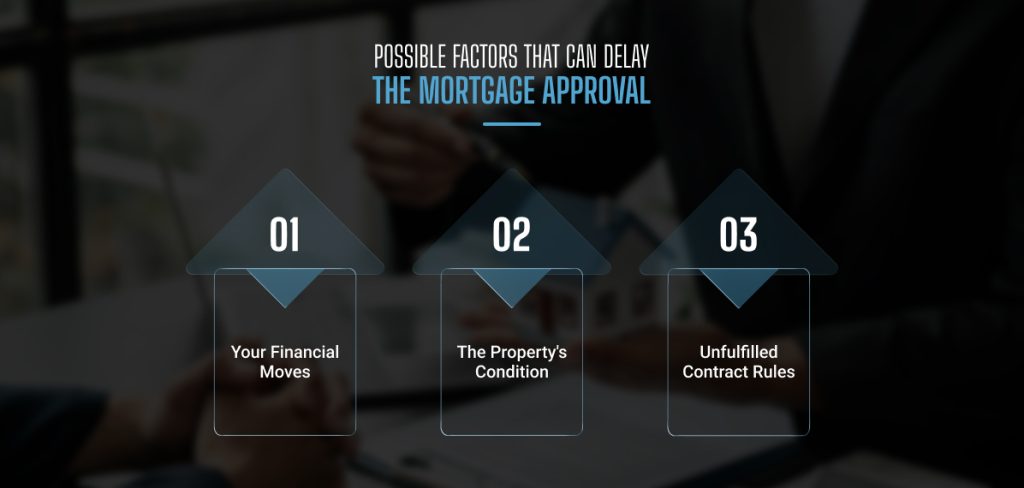

Possible Factors That Can Delay The Mortgage Approval

Getting pre-approved for a mortgage is a huge milestone. However, it does not guarantee a smooth ride all the way to the finish line.

Even with that golden ticket in hand, several unexpected speed bumps can delay or completely derail your home loan.

Once you understand the trigger, you can safeguard your final closing date.

A. Your Financial Moves

First, your personal finances must remain stable throughout this critical period. For example, making big life changes can quickly spook lenders:

- Switching jobs or experiencing sudden income changes.

- Buying big-ticket items like new cars or expensive furniture.

- Lagging on paperwork when your lender asks for extra documents.

Ultimate “What to Avoid” Financial Checklist

To protect your final loan approval, avoid these financial landmines entirely until you have the keys in hand:

- Do not buy big-ticket items like new cars, appliances, or expensive furniture on credit.

- Do not apply for, open, or close any credit cards or bank accounts.

- Do not co-sign a loan or open lines of credit for anyone else.

- Do not move large sums of money between accounts without a clear, traceable paper trail.

Do not quit your job, change industries, or transition to self-employment.

B. The Property’s Condition

Second, the house itself might cause major issues. A lender wants to ensure their investment is secure, so expect delays if:

- The home inspection uncovers major safety problems, such as mould or foundation cracks.

- The home appraisal comes in lower than the final purchase price.

- The property title shows legal bugs, such as unpaid taxes or old liens.

C. Unfulfilled Contract Rules

Finally, the absence of specific contract safety nets—known as contingencies—can ruin the deal entirely. For instance, things go wrong if you are:

- Failing to sell your current home before buying the new one.

- Missing homeowners’ insurance before the formal closing day.

Ultimately, staying financially steady and highly responsive is your absolute best strategy.

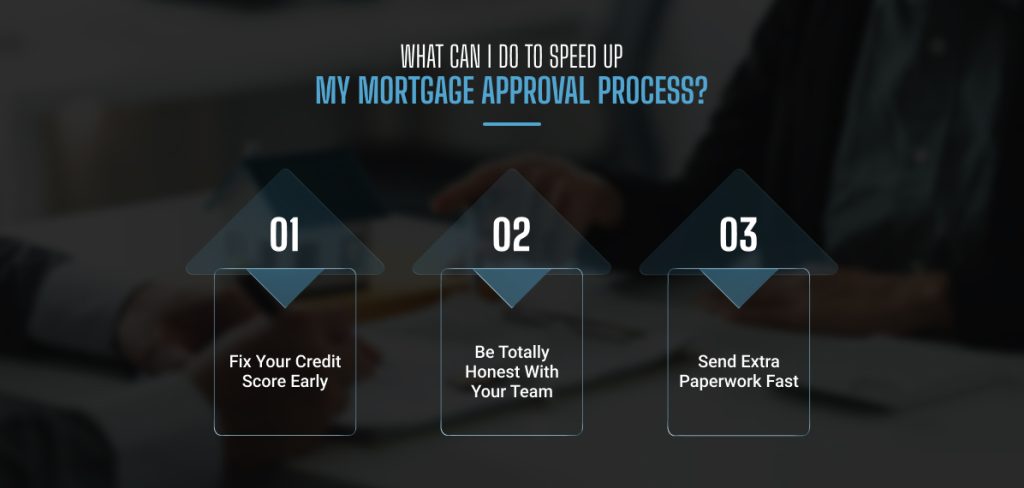

What Can I Do To Speed Up My Mortgage Approval Process?

Getting pre-approved is always a fantastic first step. However, you can do even more just to cross the finish line a little faster.

You can take a proactive approach that makes a massive difference. This can help you to speed up your home loan journey.

· Fix Your Credit Score Early

First, you should check your credit report long before you apply for a loan.

A more recent Consumer Reports Credit Checkup study found that 44% of consumers who successfully checked their files discovered mistakes.

You have to spot these errors early. This can also help you fix them before they stall your application or jeopardise your ultimate approval.

On top of that, once you know your true score, it helps you easily target the exact loans you qualify for. As a result, it can save you tons of time.

· Be Totally Honest With Your Team

Open communication with your loan officer is absolutely essential.

So, do not try to hide your financial flaws. This will only cause you major roadblocks later because underwriters always find the truth.

Therefore, it is best to disclose everything upfront, including any past late payments or additional income streams.

This builds trust early, so your team can navigate issues smoothly without any nasty surprises.

· Send Extra Paperwork Fast

Finally, expect the unexpected when it comes to documentation.

Every financial situation is unique, so your lender will likely ask for additional paperwork midway through the process.

You can keep the momentum going by taking these fast actions:

- Reply instantly to any new document requests.

- Gather basic documents, such as tax returns and pay stubs, ahead of time.

- Use digital tools to securely upload files in seconds.

You can get the keys to your new home much sooner. You just have to be honest, prepared, and lightning-fast with your paperwork.

Disclaimer: This article is for informational purposes only and does not constitute formal financial, investment, or legal advice. Always consult a licensed mortgage professional or financial advisor before making major financial decisions.

Leave A Reply