The Hidden Costs Of Retirement Properties: 8 Financial Surprises To Avoid

So, what are the hidden costs of retirement properties?

Setting aside all the great features of these properties, buyers definitely need to get to grips with costs that might include:

- Fees for selling or subletting the property.

- Little or no resale value.

- High purchase price.

- Lease restrictions.

- Very high service charges (even when the property is not occupied).

- Costly lease extensions.

- High ground rent.

Living in a specialist community seems like an ideal plan for your retirement years.

Nevertheless, these hidden financial traps have the potential to rapidly deplete your savings that you have worked so hard for if you are not vigilant.

It’s very tempting to get excited about beautiful shared gardens and friendly onsite caretakers. However, it is important to see beyond the surface.

Therefore, purchasing one of these properties is a substantial financial decision. It not only affects your retirement budget but also your family’s inheritance.

Hence, let us expose these hidden costs so that you can make a really wise, relaxed move without any worries.

What Are Retirement Properties?

First, let’s understand what retirement properties are before we discuss their financial aspects.

Basically, the design and construction methods of retirement properties are primarily for senior citizens.

These properties are available in multiple varieties. You can go for an independent house, a compact apartment, or even a traditional bungalow.

The unique feature that differentiates these homes is the inclusion of a variety of age-friendly facilities for seniors.

A majority of these developments offer luxurious shared areas such as communal gardens, libraries, restaurants, and swimming pools, as well as an on-site manager to ensure the smooth operation of the community.

Typically, the minimum age to buy these homes is 55 years. Howeve, it may vary, as some other communities set the minimum age at 60 or 70 years.

However, do remember that most of these properties are leasehold, which is one of the main factors contributing to the higher costs of retirement housing.

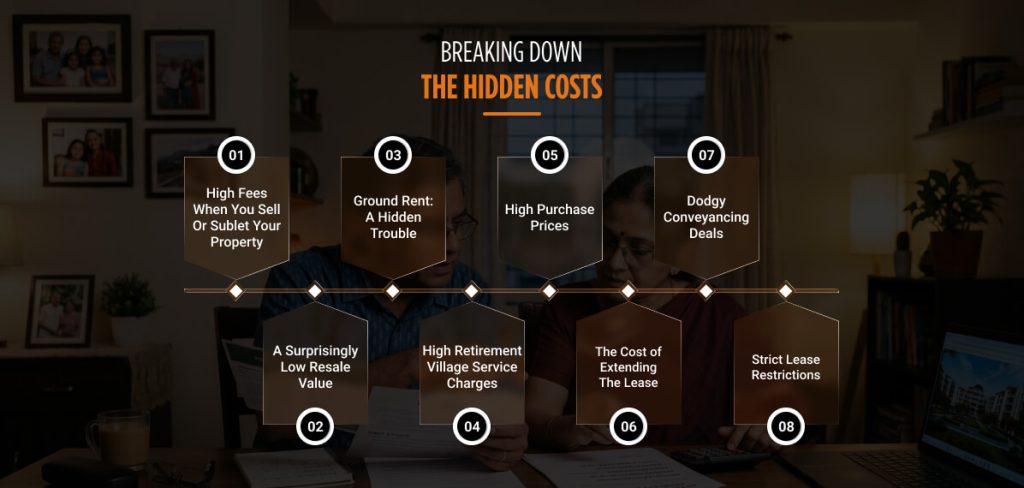

Breaking Down the Hidden Costs

Of course, the concept of retirement living is quite attractive, but the financial aspect can easily lead you down the wrong path without you realizing it.

Therefore, to save you from losing your well-earned savings, we will illustrate the first four huge hidden costs of retirement properties in the simplest possible way.

1. High Fees When You Sell Or Sublet Your Property (Exit Fees)

Most retirement leases contain an “exit fee” clause (also known as an “event” or “departure” fee), which often goes unnoticed.

This charge is applied not only when you sell the property but also when you rent it out.

In fact, you may be liable to pay even if a partner, relative, or live-in carer moves in to assist you.

• How much do they cost?

In fact, LK Partnership revealed that the average amount of those fees is almost 12%, while 1% or 2% is common.

Indeed, some upscale residences charge up to 35%.

To illustrate, London-based Riverstone Living does not hide its 35% “deferred fee.” The intention is to pay for building work and generate profit.

• Can you fight them?

Developers are obliged by certain consumer codes (ARCO, for instance) to present you with the full details.

This includes examples of those fees, before you ultimately make a purchase.

Nonetheless, once the lease is signed, the terms are set in stone. Different from usual service charges, the exit fee can’t be disputed at the legal tribunal level.

That is why it makes perfect sense to seek advice from a qualified retirement solicitor.

• Developer differences

McCarthy Stone does not view exit fees as profit but does levy a 1% “contingency fee” on the final selling price to cover window replacement and fresh decorating.

If you decide to let your apartment, they will take 1% of the annual rent. Thinking that 1% is a small amount, for a £ 400,000 dwelling, this 1% is, in fact, a hefty £ 4,000 fee.

Fortunately, Churchill Living eliminated its 1% resale fee in August 2025.

2. A Surprisingly Low Resale Value

It might seem reasonable to think that property prices always go up, but retirement housing can be a different story.

Studies reveal that around half of newly-built retirement homes sold over a decade eventually found a buyer at a loss.

To give you a real-life illustration, a family shared a very sad experience.

They bought a flat for £124, 000 in 2006, and after the owner died in 2014, it was on the market for 7 long years.

During those 7 years, the family incurred expenses of almost £16, 000 just for council tax, service charges, and ground rent on an empty flat, all that for the flat to finally sell at a low price of £60, 000 in 2021.

Before making a purchase, always research the prices at which similar properties have been sold locally.

3. Ground Rent: A Hidden Trouble

With the new legislation coming into effect in April 2023, new retirement homes in England and Wales won’t be able to charge annual ground rent anymore.

Nonetheless, if you are purchasing an older, resale retirement flat, you will most probably still be required to pay it.

This is typically £425- £500 per year, and if you fail to make a payment, eviction threats could be on the table.

If the ground rent negotiated in your agreement is excessive, it will significantly hamper the property’s future saleability.

4. High Retirement Village Service Charges

Service charges are a way to cover the building’s day-to-day operating costs, such as repairs, cleaning of shared gardens, and salaries for on-site managers.

According to a study by the website Lottie, the average weekly service charge for a retirement property is £120.93 (or £523.99 per month).

Depending on the level of luxury in your building, the amount can even exceed £1,000 every single month.

To remain on the safe side of your budget, these should be your constant actions:

• Know your stuff

Request a detailed breakdown of the service charge items and review past statements to gauge the rate of the annual price hike.

• Go over credentials

Check whether the management company is a member of a professional body, such as the Association of Retirement Housing Managers (ARHM).

• Be wary of vacant flats

When the owner dies, the family usually has to continue paying these monthly service charges until the flat is sold.

This process can sometimes last for years and accumulate to very high amounts. Luckily, certain companies offer relief.

Churchill Living, for example, allows families to stop paying service charges for up to a year if they sell their property through its agency.

5. High Purchase Prices

Buying a brand-new retirement home comes with a heavy price tag.

In fact, research from Savills shows that buyers spend about 17% more for a new-build retirement home than for a standard new-build house in the exact same area.

Part of this is down to the “new-build premium,” which means you pay a higher price for a shiny, unused property.

However, it is also because you are paying for luxury shared amenities.

Consequently, these flats will almost always cost more than a similar-sized normal home nearby.

You can often save a lot of money by researching existing flats or houses just around the corner instead.

6. The Cost of Extending The Lease

The Retirement properties are usually sold as leaseholds. Thankfully, Age UK notes that most modern retirement homes now come with 999-year leases, which completely removes the worry of having to extend them.

However, you still need to check the paperwork closely. Anything below 90 years is considered a short lease, and you should generally avoid it.

Short leases make properties incredibly hard to sell and very expensive to extend.

While the Leasehold and Freehold Reform Act 2024 is technically law, it is not yet fully up and running, meaning the old, expensive extension rules still apply for now.

7. Dodgy Conveyancing Deals

Be very careful when selecting your solicitor. If a developer tells you that they will pay your legal fees up to a certain amount and you accept their offer, think twice.

In fact, it is against the law for them to put pressure on you to use their recommended or in-house solicitor.

When buying a home for hundreds of thousands of pounds, you must be totally sure that your solicitor is completely independent and is working solely in your best interests.

8. Strict Lease Restrictions

Always remember to check the building rules carefully before signing a deal.

Many times, retirement lease agreements have very strict restrictions, for instance, pet bans or prohibitions on subletting the property.

You may have a serious problem if there is a hidden cost, as you cannot rent the property out.

If the flat stays empty, this can be the case, especially when you still have to pay monthly service charges.

Likewise, be sure to note the minimum age requirements (which can range from 55 to 70).

As a result, this might prevent younger family members or carers from coming to you in the future.

Things You Should Know

• Health

It’s also wise to think about your needs in case you one day need a doctor or a carer 24 hours a day.

While some retirement communities have care professionals ready to assist, others do not, and this could result in another move for you.

• University And Lifestyle Opportunities

Having excellent facilities at the flick of a switch is great, but retirement villages do not suit everyone’s lifestyle.

Some residents feel the rooms are way too small for them.

Whereas some individuals oppose the idea of aging exclusively among a population of the same age.

Costs, Benefits, and Smart Alternatives

Let’s consider the actual purchase prices, the perks thrown in, and some smart moves if you’d fancy giving the hidden costs of retirement properties a miss.

How Much Do They Cost to Buy?

Prices vary widely by location and developer. Based on Lottie, the comprehensive data source, here is the average price message:

- In London, a one-bedroom flat is priced at about £ 708,200, while the jump to a two-bedroom property increases the price to around £ 800,000.

- In the North of England, the cost of things is considerably less. A one-bedroom apartment costs an average of £ 215,922, and a two-bedroom apartment is priced at around £ 304,135.

What Are the Benefits?

These villages, despite the high prices, do provide great lifestyle benefits:

- Enhanced Security: Buying in a secure complex is generally associated with greater safety and reduced loneliness compared to living entirely alone.

- Maintenance-Free Living: Developers not only handle major maintenance but also handle day-to-day repairs. However, you will have to pay for the service.

- Support Available: Customized care or assisted living is generally provided in most villages.

This means you can maintain your independence and get the help you may need, with minimum disruption.

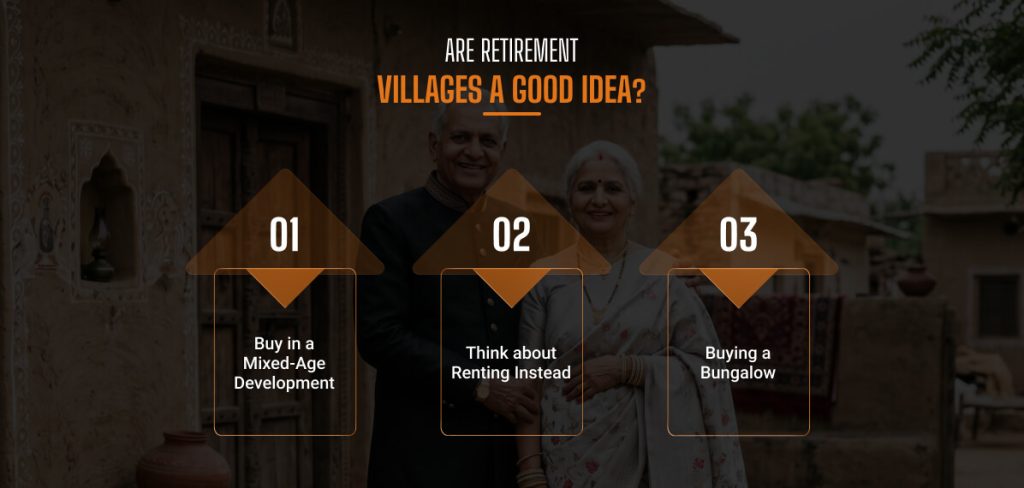

Are Retirement Villages a Good Idea?

Seriously, it is a good idea to consider your own life before making a decision. You can be easily drawn in by glossy brochures and persuasive salespeople.

Our main point is to advise you to do your own research so that you know exactly what you are signing up for.

Maybe the advantages will entice you and ignore the drawbacks of the high costs, or you might simply decide to walk away.

Three Great Alternatives to Consider

• Buy in a Mixed-Age Development

Consider buying in a general, regular residential development. In fact, many city developments offer excellent facilities such as swimming pools, a concierge, restaurants, etc.

You will pay service charges, but completely avoid the dreadful exit fees. Besides, you will enjoy the company of individuals of various ages.

• Think about Renting Instead

There is a way to experience a retirement community by renting a flat there.

When you rent, you will have to pay the service charge regularly, but you will be free of the huge exit fees.

The catch is that if you are selling your main home to fund this, it is advisable to seek professional financial advice.

In the event that either you or your partner might need to move into a care home and/or require care services, the money realized from the house sale will be counted as savings and used towards care.

• Buying a Bungalow

There are not many bungalows. They can be expensive, but they offer a perfect walk-in, walk-out layout without stairs.

Besides, bungalows are much more peaceful and private than living in a busy residential development. Usually, they come with larger gardens and wider plots.

Who Are the Main Developers?

If you want to look at options directly, the biggest private retirement builders in the UK are:

- McCarthy Stone

- Churchill Living

- Guild Living

- Inspired Villages

- Audley Retirement

- Anchor Hanover

You can easily find their listings directly on their websites or by filtering for retirement homes on Rightmove and Zoopla.

Leave A Reply